About MCarloRisk3DLite

Drift-diffusion Monte Carlo forecaster from raw asset price data including crypto assets, with bulk backtesting.

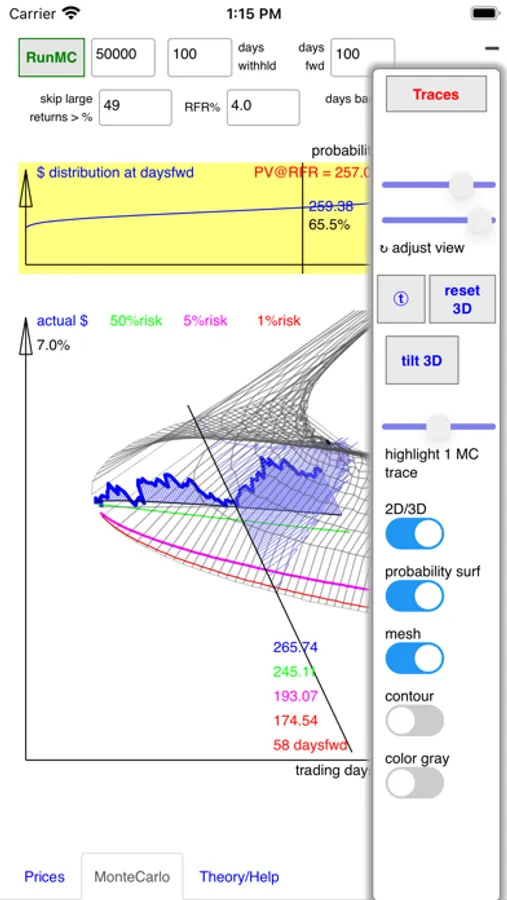

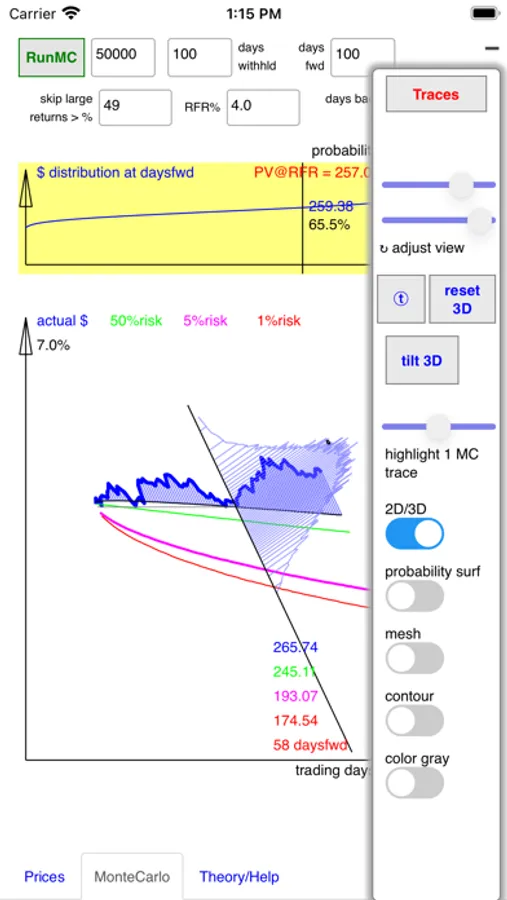

This Lite version of the app now supports 3D views on iPhones, with hidden control menu to give more

space for the graphics. Use + button on upper right of the Monte Carlo tab view to show additional controls.

It allows an introduction to these methods without an undue amount of options to avoid confusion.

See MCarloRisk3D for iPad and macOS for Full Featured Functionality.

The simplified Lite version of the app is also made available on iPad.

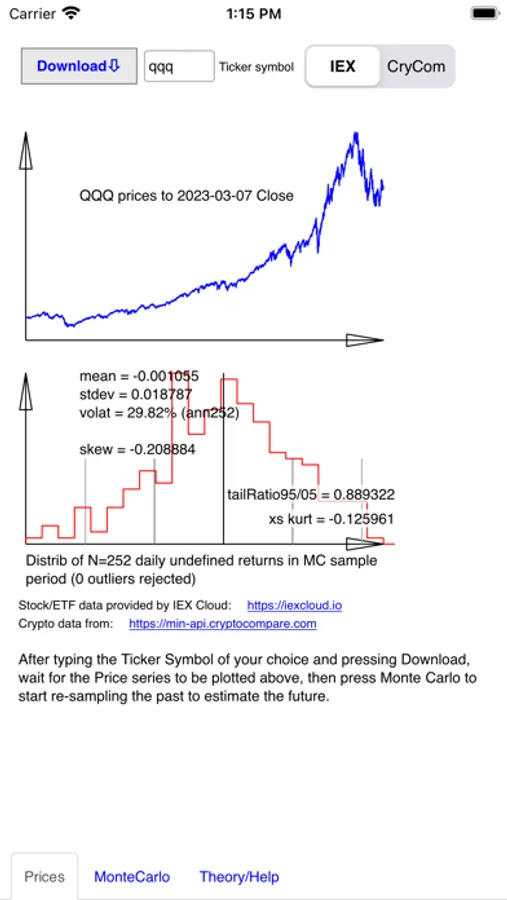

Instead of time series (traditional charting), the app is based on the statistical properties of daily return data (percent change in asset price per trading day).

- examine historical returns distributions for one asset at a time, with distribution metrics computed automatically such as mean return, volatility, skew (bullish/bearish), kurtosis (fat tail metric), and tail ratio (fat tail bias: bullish or bearish)

- display returns as a histogram along with these return metrics

- generate monte carlo forecast models from empirical (actual) historical returns data, without assuming normality of returns

- backtest these models in a single pass bulk backtest

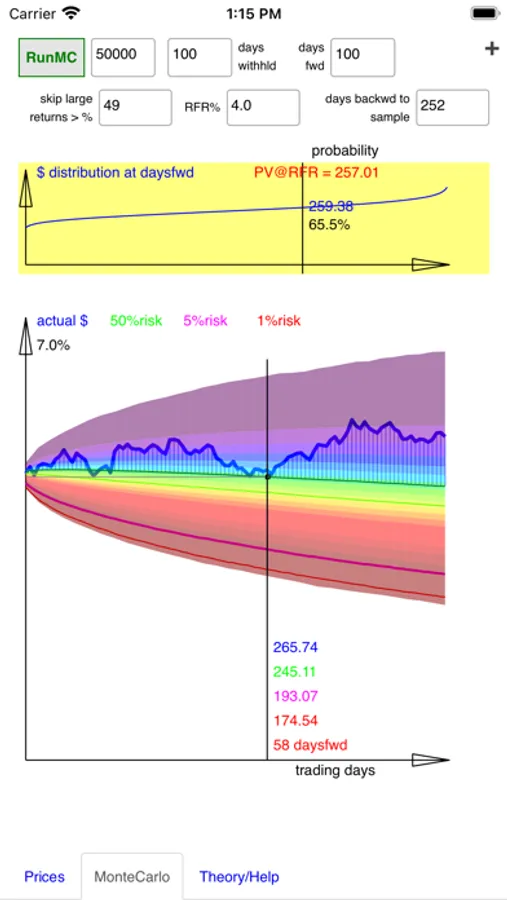

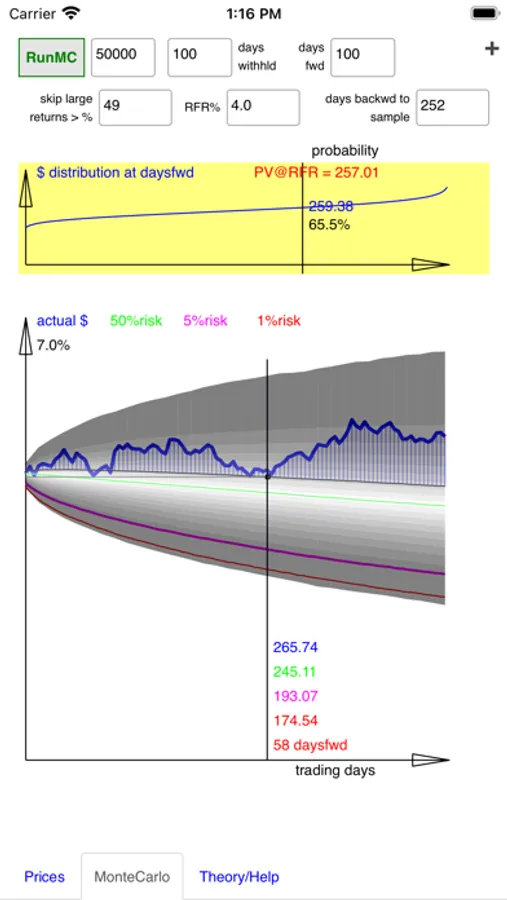

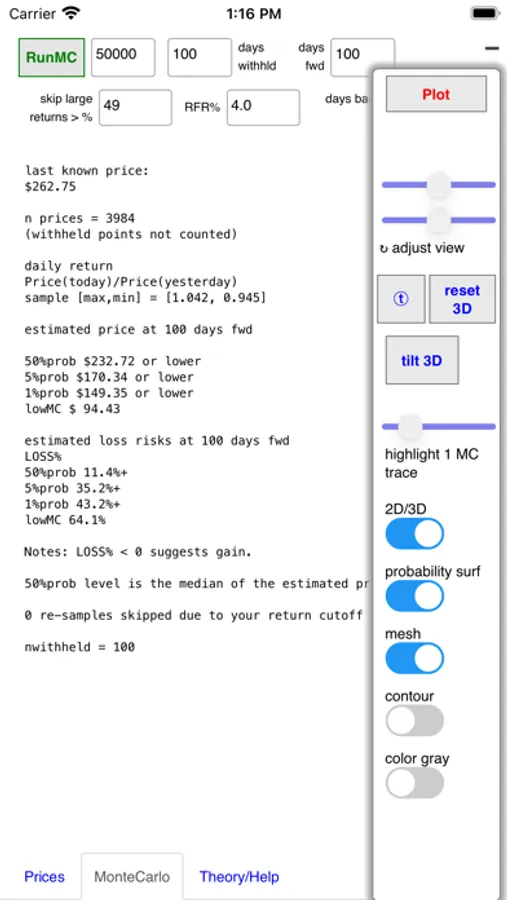

- get simple metric report-outs and detailed envelope graphs of forecast results, optionally displayed as a 3D surface for easier understanding

This app resamples from empirical daily returns to generate forward-in-time monte carlo paths (random walks).

No distribution shape assumptions are needed, works with empirical returns distribution (historical data as-is). This is especially useful for new assets such as crypto or more exotic equities which may not conform to normal or lognormal return assumptions, especially in shorter time periods.

Aggregates monte carlo paths into a (price, time, probability) surface. Allows user to slice thru and examine this surface (e.g. price over time versus probability) and visualize the surface in 3D and with shaded contour plots.

Allows user to set up bulk backtests by withholding the most recent data and examining the model versus this withheld data.

Allows display of a sampling of monte carlo random walk paths before they are aggregated, allowing highlighting of individual paths; for teaching and example purposes.

Detailed training and examples available online in the Help tab.

Raw price data from IEX Exchange or cryptocompare.com

This Lite version of the app now supports 3D views on iPhones, with hidden control menu to give more

space for the graphics. Use + button on upper right of the Monte Carlo tab view to show additional controls.

It allows an introduction to these methods without an undue amount of options to avoid confusion.

See MCarloRisk3D for iPad and macOS for Full Featured Functionality.

The simplified Lite version of the app is also made available on iPad.

Instead of time series (traditional charting), the app is based on the statistical properties of daily return data (percent change in asset price per trading day).

- examine historical returns distributions for one asset at a time, with distribution metrics computed automatically such as mean return, volatility, skew (bullish/bearish), kurtosis (fat tail metric), and tail ratio (fat tail bias: bullish or bearish)

- display returns as a histogram along with these return metrics

- generate monte carlo forecast models from empirical (actual) historical returns data, without assuming normality of returns

- backtest these models in a single pass bulk backtest

- get simple metric report-outs and detailed envelope graphs of forecast results, optionally displayed as a 3D surface for easier understanding

This app resamples from empirical daily returns to generate forward-in-time monte carlo paths (random walks).

No distribution shape assumptions are needed, works with empirical returns distribution (historical data as-is). This is especially useful for new assets such as crypto or more exotic equities which may not conform to normal or lognormal return assumptions, especially in shorter time periods.

Aggregates monte carlo paths into a (price, time, probability) surface. Allows user to slice thru and examine this surface (e.g. price over time versus probability) and visualize the surface in 3D and with shaded contour plots.

Allows user to set up bulk backtests by withholding the most recent data and examining the model versus this withheld data.

Allows display of a sampling of monte carlo random walk paths before they are aggregated, allowing highlighting of individual paths; for teaching and example purposes.

Detailed training and examples available online in the Help tab.

Raw price data from IEX Exchange or cryptocompare.com

MCarloRisk3DLite Screenshots

Tap to Rate: